The staff retention rate within the Cambodian microfinance sector remains high, with the latest figures reflecting a positive working environment and competitive benefits among the member institutions of the Cambodia Microfinance Association (CMA). This trend indicates that the vast majority of employees continue to build long-term careers within the country's microfinance industry.

The staff retention rate measures the percentage of workers who remain at a company or within a specific sector over a set period. It serves as a key indicator of worker satisfaction and an organization's effectiveness in preventing talent loss.

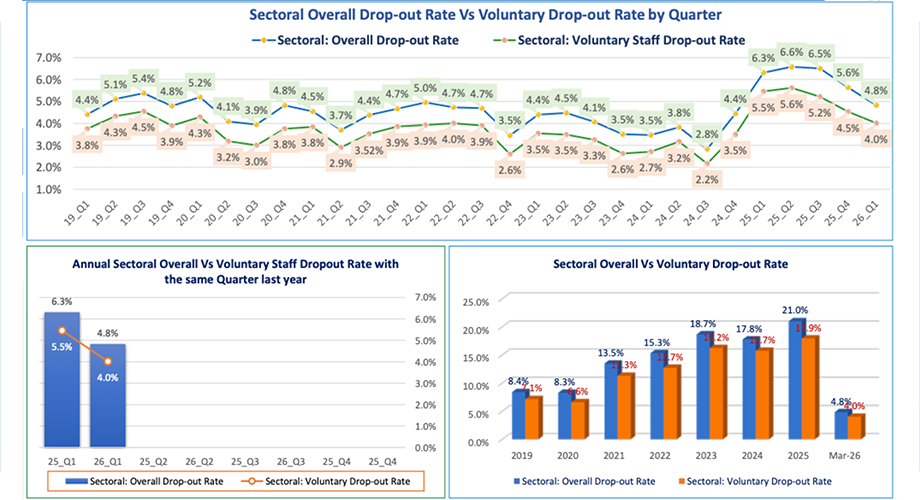

The CMA’s Employee Turnover Ratio Report shows among the 109 members that submitted reports for Q1 2026—including banks, Microfinance Deposit-taking Institutions (MDIs), Microfinance Institutions (MFIs), Financial Leasing Institutions (FLIs), and Rural Credit Institutions (RCIs)—the employee retention rate stood at 95.2% as of March 31, 2026.

The report highlights that this retention rate represents a 0.8 percentage point increase from the fourth quarter of 2025 and a 1.5 percentage point increase compared to the first quarter of 2025. By institution type, MDIs reported a retention rate of 95.6%, MFIs recorded 93.1%, FLIs achieved the highest retention rate at 95.9%, and RCIs recorded the lowest retention rate at 87.8% during the same period.

Furthermore, the report provides encouraging evidence regarding the overall turnover rate which stood at 4.8% with 4% voluntary turnover rate in first quarter of 2026. Both indicators improved compared to the fourth quarter of 2025. Specifically, the overall turnover rate decreased from 5.6% to 4.8%, while the voluntary turnover rate fell from 4.5% to 4.0% during the same period.

The data also illustrates that staff mobility varies across different categories of financial institutions. These variations are expected, given that each institution operates under distinct business models, geographic footprints, and workforce requirements. Rather than viewing turnover as a standalone metric, institutions are encouraged to interpret it alongside recruitment, staff development, productivity, and employee engagement to gain a comprehensive picture of organizational health.

As Cambodia's financial sector continues to evolve, attracting and retaining skilled professionals will remain a core strategic priority. The latest turnover data demonstrates that the microfinance industry has maintained a resilient workforce, providing a solid foundation for sustainable growth and continued service to communities across the country.